An Unexpected Result

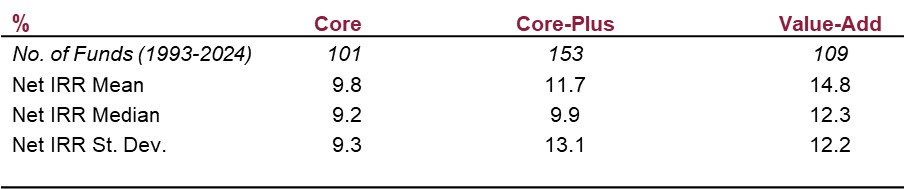

An analysis of the historical performance of all infrastructure funds in the Preqin database across core, core-plus, and value-add strategies challenges conventional expectations. It could be expected that value-add strategies, which promise greater return but inherently carry higher risk, would display a wider return dispersion of fund performance compared to their lower risk / return counterparts across vintages. However, an analysis of historical performance reveals an unexpected pattern. Core strategies, as expected, provided the most stable return proposition across vintages, but value-add funds offered a lower return dispersion combined with a higher return than core-plus funds.[1]

Infrastructure Funds, Net IRR Return Analysis

Source: Preqin database, analysis includes full dataset across all fund vintages (1993-2024), excludes top 3 performing and worst 3 performing funds by strategy (outliers). Past performance is not indicative of future returns. [2]

What’s going on:

As an asset class, core-plus is broad, and includes the highest number of funds in the database. Strategies have evolved over time to focus on a diverse mix of geographical and sector propositions, as well as on assets across various development stages. Nevertheless, core-plus assets may typically focus on assets with longer duration cash-flows and have a yield element compared to value-add assets. So, on an individual asset basis, value-add assets may experience wider return dispersion compared to individual core and core-plus assets, as they rely more on exits for value creation.

However, fund-level diversification tends to smooth out volatility of individual assets for value-add strategies.[3] This is likely a result of value-add assets typically having lower exposure to systematic risks than core-plus assets, particularly long-term interest rate changes across macroeconomic cycles. Value-add assets are more exposed to idiosyncratic risks, particularly business risk or development risk. This can support portfolio diversification at the fund level, due to the low performance correlation across assets in a fund, which can contribute to reducing overall fund performance volatility.[4]

Distribution of Infrastructure Funds Returns By Strategy

Source: Preqin database, includes full dataset across all fund vintages (1993-2024), excludes top 3 performing and worst 3 performing funds by strategy (outliers) for data normalisation purposes. Past performance is not indicative of future returns.

Downside & upside risks:

Looking at the return distributions across strategies, value-add funds also appear to have exposed investors to less downside risk historically. Compared to core and core-plus strategies, a lower proportion of value-add funds displayed returns below 6%, and the strategy appears also more positively skewed in comparison to the highest share of funds returning above 14%. These findings suggest that by adopting a diversified allocation across multiple value-add funds and managers along with a multi-vintage investment approach, investors would have historically captured the strong risk-adjusted market performance (beta) of value-add strategies, while mitigating the risk of excessive return dispersion.[5]

Authored by:

Gianluca Minella

Head of Research

References

[1] Based on an analysis of net IRRs across all vintages for funds available in the Preqin database. Past performance is not indicative of future returns.

[2] Net IRRs include the impact of fund-level borrowing through subscription facilities. Net IRR may be favourably impacted when the fund uses its line of credit to facilitate investments, or to make follow-on investments in such companies, because it defers the calling of capital from investors. Since IRR is calculated as of the date the investors’ capital is called, rather than at the earlier time of funding the portfolio company purchase or follow-on investment, the use of a line of credit may have a favourable impact on performance returns and may not reflect the actual return an investor would achieve without the leverage effect. To the extent that expenses of the subscription facility do not fully offset this leveraging effect, IRRs experienced by investors and presented herein will be higher than IRRs experienced by the fund.

[3] Based on IRCP proprietary database of infrastructure transactions, as at December 2024. Past performance is not indicative of future returns. There is no guarantee that the forecast highlighted may materialise.

[4] InfraRed Capital Partners, Value-Add Infrastructure, December 2024.

[5] Past performance is not indicative of future returns.

InfraRed has based this document on information obtained from sources it believes to be reliable, but which have not been independently verified. All charts and graphs are from publicly available sources or proprietary data. Except in the case of fraudulent misrepresentation, InfraRed makes no representation or warranty (express or implied) of any nature or accepts any responsibility or liability of any kind for the accuracy or sufficiency of any information, statement, assumption or projection in this document, or for any loss or damage (whether direct, indirect, consequential or other) arising out of reliance upon this document. InfraRed is under no obligation to keep current the information contained in this document.

You are solely responsible for making your own independent appraisal of and investigations into the products, investments and transactions referred to in this document and you should not rely on any information in this document as constituting investment advice. This document is not intended to provide and should not be relied upon for tax, legal or accounting advice, investment recommendations or other evaluation. Prospective investors should consult their tax, legal, accounting or other advisors. Prospective investors should not rely upon this document in making any investment decision.

Investments can fluctuate in value, and value and income may fall against an investor’s interests. The levels and bases of taxation can change. Changes in rates of exchange and rates of interest may have an adverse effect on the value or income of the investment or any potential returns. Figures included in this document may relate to past performance. Past performance refers to the past is not a reliable indicator of future results. There can be no assurance that the opportunity will achieve its target returns or that investors will receive a return from their capital. Investment in the products or investments referred to in this document entails a high degree of risk and is suitable only for sophisticated investors who fully understand and are capable of bearing the risks of such an investment, including the risk of total loss of capital originally invested. It may also be difficult to obtain reliable information about the value of these investments, which will often have an inherent lack of liquidity and will not be readily realisable.

This document is being issued for the purposes of providing general information about InfraRed’s services and/or specific assets and their operational performance only and does not relate to the marketing of investments in any alternative investment fund managed by InfraRed.

InfraRed may offer co-investment opportunities to limited partners, or third parties. These circumstances represent conflicts of interests. InfraRed have internal arrangements designed to identify and to manage potential conflicts of interest.

This document should be distributed and read in its entirety. This document remains the property of InfraRed and on request must be returned and any copies destroyed. Distribution of this document or information in this document, to any person other than an original recipient (or to such recipient’s advisors) is prohibited. Reproduction of this document, in whole or in part, or disclosure of any of its contents, without prior consent of InfraRed or an associate, is prohibited.

This document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

InfraRed Capital Partners is a part of SLC Management which is the institutional alternatives and traditional asset management business of Sun Life.